Serviços Personalizados

Journal

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Acessos

Acessos

Links relacionados

-

Similares em

SciELO

Similares em

SciELO

Compartilhar

Permalink

PermalinkTourism & Management Studies

versão impressa ISSN 2182-8458

TMStudies vol.11 no.1 Faro jan. 2015

MANAGEMENT – RESEARCH PAPERS

Are companies less environmentally-friendly due to the crisis? Evidence from Europe

¿Son las empresas menos respetuosas con el medioambiente durante la crisis? Evidencia europea

María del Mar Miras-Rodríguez1; Bernabé Escobar-Pérez2; Amalia Carrasco Gallego3

1University of Extremadura, Faculty of Business Studies and Tourism, Department of Financial Economics and Accounting, Avd. de la Universidad S/N, 10003, Cáceres, Spain, mmiras@unex.es

2University of Seville, Faculty of Economics and Business Studies, Department of Accounting and Finance, 41018, Spain, bescobar@us.es

3University of Seville, Faculty of Economics and Business Studies, Department of Accounting and Finance, 41018, Spain, agallego@us.es

ABSTRACT

Academicians and managers are worried about what is going to happen with the Environmental Responsibilities of companies due to the worsening of their financial situation caused by the severe economic crisis that is significantly affecting them. The aim of this paper is to study the effect of the crisis on the environmental behavior of companies from the European countries that are suffering the financial crisis most (Greece, Ireland, Italy, Portugal, and Spain) through a data panel study between 2005 and 2012.

The results show surprisingly that proactive, environmentally-friendly actions have not decreased during the crisis but rather that the crisis has meant an increase in environmental commitment. This is strongly motivated by the Product Innovation actions which attain the highest increase.

Keywords: Environmental responsibility, crisis, performance, Data Panel, Europe.

RESUMEN

Las consecuencias que la crisis económica pueda tener sobre la responsabilidad medioambiental de las empresas preocupan tanto a directivos como a académicos. Por ello, el objetivo de este trabajo es estudiar el efecto que la crisis está teniendo sobre los comportamientos medioambientales de las empresas, en particular, de los países europeos que más están sufriendo la crisis (España, Grecia, Irlanda, Italia y Portugal) a través de un estudio de datos de panel (2005-2012).

Los resultados muestran que las acciones medioambientalmente proactivas no han disminuido durante la crisis, sino que por el contrario, la crisis ha supuesto un incremento en el compromiso ambiental de las empresas. Ahora bien, es necesario señalar que estos resultados están fuertemente determinados por las acciones relativas a la Innovación en los Productos, ya que son éstas las que han experimentado el mayor incremento.

Palabras clave: Responsabilidad medioambiental, crisis, rendimiento, datos de panel, Europa.

1. Introduction and objectives

Companies are not unaware that the current financial and economic crisis is being singular given its intensity, complexity and the difficulties that some developed countries are having in overcoming it. This is due to its huge consequences. These range from the closing down of several firms, financial losses, or, at best, a large reduction of profits (Miras, Carrasco & Escobar, 2014).

Since the current economic crisis emerged, the priorities of business have changed and liquidity management has become one of the most important aspects to consider in each decision. Therefore, financial difficulties have forced firms to redefine their business and implement austerity plans as a unique alternative to survive. They have therefore reduced expenses (Karaibrahimoglu, 2010), delayed many Corporate Social Responsibility (CSR) initiatives and/or revoked their social and environmental responsibilities (Orlitzky, Schmidt & Rynes, 2003).

Yet, on the contrary, during these rough times carrying out CSR actions is more necessary than ever (Karaibrahimoglu, 2010) because of the greater needs. Additionally, society is even more concerned and reacts more to the companies CSR engagement and customers value more those firms which are committed to CSR (Molina-Azorín, Claver-Cortés, López-Gamero & Tarí, 2009). Hence, companies are asked to be more involved in supporting social and environmental causes (Grigore, 2011).

These CSR behaviors are usually grouped into Social, Environmental and Economic actions (Triple Bottom Line approach- Elkington, 1998), and several researchers have shown the appropriateness of differing CSR from environmental actions (Bansal & Gao, 2006) since the former are more technical, have their own reporting criteria, and are highly regulated (Endrikat, Guenther & Hoppe, 2014).

Despite the environmental regulation, nowadays it is not sufficient for firms to comply with the law (Pérez-Calderón, Milanés-Montero, Meseguer-Santamaria & Mondejar-Jimenez, 2011) and they have to exceed the legal requirements (proactive environmental actions – Buysse & Verbeke, 2003) and this involves making significant investments. This means that CSR actions can be the hardest hit by the crisis due to their voluntary implementation.

Additionally, Environmentally Responsible Actions are made up of different kinds of actions that are mainly Emission Reduction (Hart & Ahuja, 1996; King & Lenox, 2001), Product Innovation (Porter & Van der Linde, 1995; Albertini, 2013), and Resource Reduction (Al-Tuwaijri, Chistensen & Hughes, 2004; Pérez-Calderón et al., 2011) and whose costs are diverse. When the company is involved in its environmental responsibilities, the Emission Reduction (ER) and Resource Reduction (RR) actions require more and more up-front investments in training and equipment (Hart & Ahuja, 1996), while Product Innovation (PI) actions could reduce inefficiencies and improve industrial competitiveness in a less expensive way (Porter & Van der Linde, 1995). Additionally, there is some lag between the initiation of new ER and RR actions and their associated cost savings or benefits (Hart & Ahuja, 1996). All this evidence makes it necessary to study each of them separately, since they could be affected in a different way during the crisis.

In this context, the current financial crisis provides a perfect opportunity to test the real commitment of the companies toward the CSR approach, and allows a better understanding of what their real motivations or interests are when behaving in an environmentally responsible way. Therefore, the aim of this paper is to study how environmentally responsible actions are going to be influenced by these extraordinary financial circumstances.

If companies only implement this kind of actions looking for legitimacy or direct benefits (short-term vision), the Environmentally Responsible actions should be drastically affected by the crisis due to the high cost of implementation. However, if organizations are really engaged with these issues and they have actually integrated them into their business strategy, they could take advantage of the crisis as an opportunity instead of considering it as a great threat (Fernández, 2009). Therefore, the present crisis may not directly mean the disappearance of environmentally responsible actions, although their number could be reduced and/or the kind of actions may change, with those that are less expensive gaining more importance.

Despite the relevance of this issue, few researchers have addressed the problem worldwide (Charitoudi, Giannarakis & Lazarides, 2011), or in specific countries (Ducassy, 2013). Nevertheless, it is particularly interesting to test this puzzle in the European countries most affected by the economic downturn - Greece, Ireland, Portugal, Spain and Italy (Santos, Anunciação & Jesus, 2013) - because we can find out if they are really committed to these actions or not.

Therefore, we are going to analyze if companies from the European countries that are suffering the crisis most continue behaving in an Environmentally Friendly way (proactive), through a data panel study from 2005 until 2012.

The results show that the proactive environmentally-friendly actions carried out have not decreased during the crisis but rather that the crisis has meant an increase in environmental commitment. This is strongly motivated by the Product Innovation actions which attain the highest increase.

The rest of the paper is organized as follows. In Section 2, we focus on the debate about the theoretical framework. In Section 3, we look more closely at the sample and variables used, as well as the methodologies employed. Section 4 presents the results of our study and the discussion. Finally, in Section 5 we show the conclusions, the limitations of the study and some of the lines of investigation which remain open.

2. Literature review

Despite the importance given to CSR in the literature and its wide acceptance in the business world, the crisis has prompted it being called into question. This is particularly so for environmental actions since social needs become a priority during rough times.

As was discussed by Aragón-Correa (1998), the environmentally-friendly actions of companies can be reactive or proactive, and this fact is undoubtedly going to influence their relationship to the company´s performance (King & Lenox, 2002). On the one hand, reactive environmental actions whose objective was to comply with the regulation (Russo & Fouts, 1997) could not be stopped despite the crisis. However, proactive and voluntary policies (those that go beyond compliance) are the perfect target for the crisis.

Even though the relationship between Environmental actions and performance has been widely discussed in the specialized literature through several literature reviews (Molina-Azorín et al., 2009) and meta-analyses (Dixon-Fowler, Slater, Johnson, Ellstrand & Romi, 2013; Albertini, 2013; Endrikat et al., 2014), these are mainly focused on the effect on performance of the implementation of several environmental proactive actions (Endrikat et al., 2014).

However, the contrary causal relationship (the effect that the companies financial situation has on the proactive environmental actions) has also received less attention, although it has been theoretically supported by several Theories and Hypotheses.

According to Waddock and Graves (1997), companies will be more or less environmentally responsible depending on the availability of their financial resources. Achieving a better performance will allow great investments in proactive environmental projects to be made. Consequently, being environmentally-friendly is only viable in financially healthy companies.

Moreover, the Managerial Opportunism Hypothesis reported by Williamson (1965) -an extension of the Agency Theory (Ross, 1973) - discussed that considering that the purposes of managers may be different from those of shareholders and other stakeholders, managers' objectives will be oriented toward the short-term and immediate profitability (Baptista, Matias & Valle, 2013). In accordance with this, the high cost of Environmental initiatives would be responsible for a drastic reduction of this kind of proactive actions. This is because managers worried by the financial situation prefer to decrease all costs whose short-term benefits they are not sure about, since their main concern is their survival in the company. Hence, the present financial situation would trigger a large decrease of environmental activities or policies.

Notwithstanding, as some mechanisms (financial rewards, shares) were specified in order to avoid managerial opportunism (Miller, 2002), the shareholders interest has to be taken into account (Eisenhardt, 1989). In addition, during a crisis period, directors and shareholders should come to an agreement about the companies strategic decisions. Managers pressured by shareholders could thus choose continuing with CSR policies because they understand that it may be a good way to manage the economic crisis and they may be more concerned about long-term repercussions. Therefore our hypothesis is:

H1: Despite the crisis, companies continue to behave in an environmentally responsible way.

Based on the evidence that each kind of Environmentally-friendly actions (ER, RR and PI - Porter & Van der Linde, 1995; Hart & Ahuja, 1996; King & Lenox, 2001; Al-Tuwaijri, et al., 2004; Albertini, 2013) requires a different level of investment and the existence of time lags in profits or cost savings (Hart & Ahuja, 1996), we expect that the crisis is not going to affect to all of them in the same way. Particularly, we expect that PI actions are those which are showing an increase during these tough times, although the cost savings of the ER and RR actions should be even more important.

3. Methodology

The population under study are companies listed in Greece, Ireland, Italy, Portugal and Spain, since these are the European countries which have been most affected by the financial and economic crisis, as they were intervened by the European Union (Santos et al., 2013; Sánchez-Vargas, 2014) or they have had extremely high risk premia.

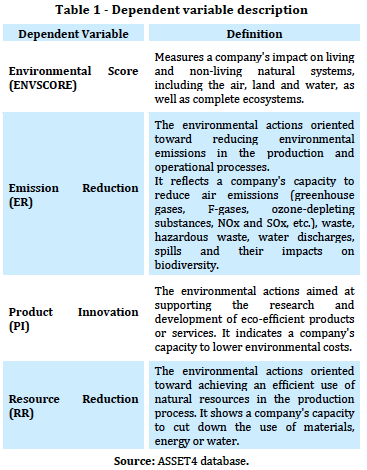

Not all the companies provide Environmental data, so the final sample was made up of 130 firms whose data have been provided by ASSET4 (Environmental Score: Emission Reduction, Product Innovation, and Resource Reduction) and the DataStream Professional Database (financial data and control variables).

The dependent variables used in the study are the Environmental Score, the Emission Reduction Score, the Product Innovation Score and the Resources Reduction Score (Table 1). The ASSET4 database has already been used for this purpose by Ioannou and Serafeim (2012), due to its being much employed by investors to build their sustainability reports. It provides a collection of indicators (valued from 0 to 100) organized into four pillars: Social Scores, Environmental Scores, Corporate Governance Scores and, finally, Economic Scores.

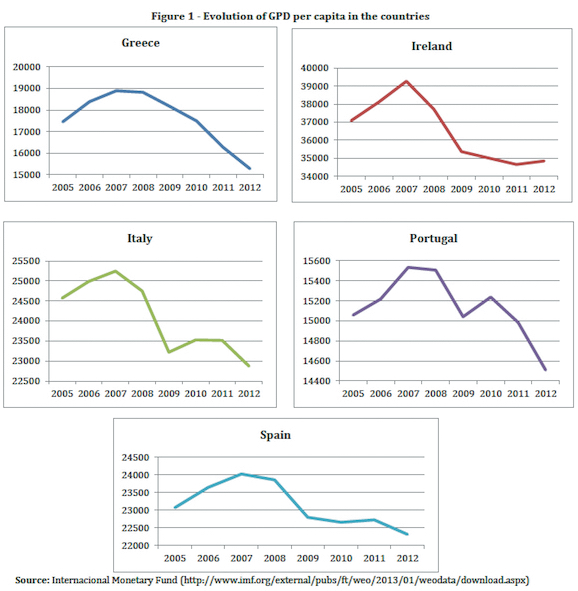

As independent variables, we are going to use a crisis variable (dummy) and the return on assets (ROA) ratio. The crisis variable reflects if the year studied is before or during the crisis depending on each countrys evolution of GDP per capita (Figure 1). When the GPD per capita starts to decrease in each country, this variable takes value 1, while it takes value 0 before this decrease. Considering the evidence of Figure 1, we conclude that the first year of the financial and economic crisis is 2008 in all the countries.

According to the evidence found by Orlitzky et al. (2003), accounting measures – especially ROA -are those that best reflect the performance-return of the CSR actions- Finally, we introduce several control variables, such as the size of the company (Ln Total of Assets), the leverage level, the industry, the market (country), and the previous Environmental Score, in accordance with the previous literature (Waddock & Graves, 1997; McWilliams & Siegel, 2001).

To achieve our aim, we are going to obtain some descriptive statistics and to estimate several panel data random regression models.

4. Results and discussion

As mentioned previously, the aim of the paper is to study how each kind of environmentally responsible actions is going to be influenced by the crisis.

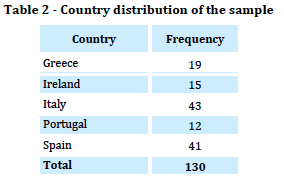

Firstly, we show the sample distribution of countries and industries (Tables 2 and 3). As can be seen in Table 2, there are two countries (Italy and Spain) that contribute at least 65% of the sample, while the rest was from Greece, Ireland, and Portugal.

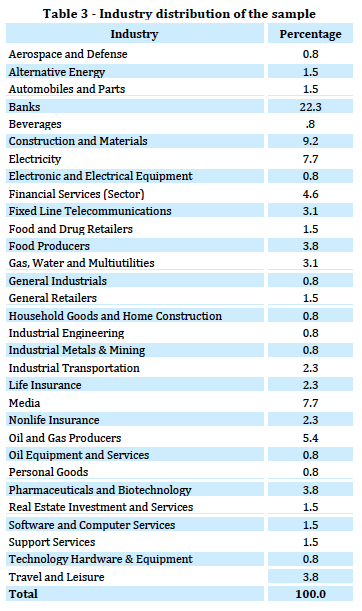

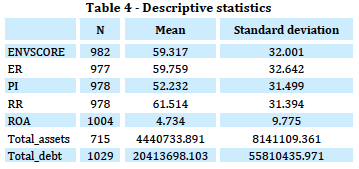

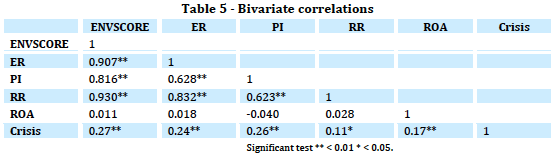

Regarding the sectors, 26.9% of the sample is dedicated to financial services, 18.5 % to energy, 9.2% to construction and 7.7% to media. Other industries have little presence in the sample. We report the sample descriptive statistics (Table 4) and the bivariate correlations between all the variables included in the study (Table 5).

From the statistics shown in Table 4, we identify that the Environmental Score and the ER variables behave in a very similar way (mean value and variability). The RR actions present the highest score, while PI is the dependent variable which shows the lowest value. As there is a considerable variation in firm size and debt (according to the Standard deviation value), it is necessary to include these variables in the study to control those aspects.

From Table 5, we observe that there is a significant positive correlation between all the Environmental variables. Though no significant correlation is reported between the Environmental variables and ROA, the correlation of all the variables (Environmental and ROA) with the crisis is positive and statistically significant.

Finally, Figure 2 denotes the mean evolution of the dependent variables. From this, we begin to deduce that the Environmental Responsibility of businesses not only has not decreased during the crisis but has in fact increased. This evidence will have to be supported by the results of the multivariate test.

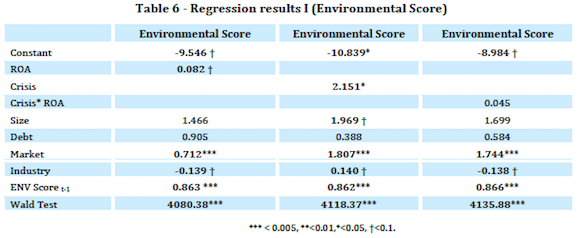

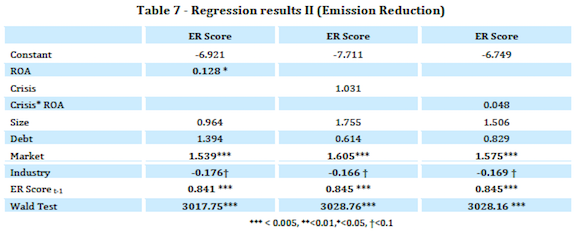

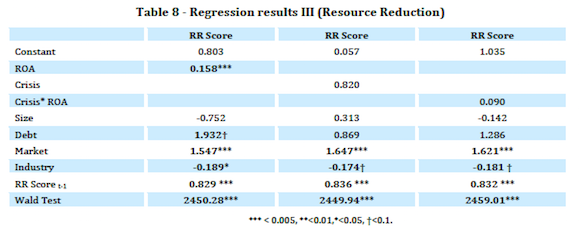

The results of the ER and RR regressions (Table 7 and 8) show the positive and direct influence that ROA has on these Environmental variables (more significant in RR), although it seems that the financial and economic crisis is not having any significant effect on them. In this sense, companies which are engaged in that field and which made important investments in it continued being committed, although such investments could be reduced during these tough times.

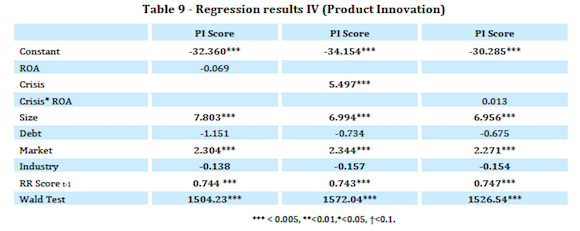

Furthermore, the tests of the control variables are statistically significant for the market and industry in Tables 6, 7 and 8. However, the results of the PI differ from the others (Table 9) because the ROA attained by the company is not determined by it. That is, the good or bad results achieved by the company are not influencing the PI actions.

Nevertheless, the crisis shows a great effect on it. That is, during hard times the PI increases, while during good periods it decreases. Additionally, the company´s size is a determinant of this relationship (bigger companies tend to innovate more), as well as the market in which each company operates.

5. Conclusions

The aim of the paper is to analyze how each kind of environmentally responsible action is going to be influenced by the current financial and economic crisis. To do so, we studied the environmentally-friendly actions carried out from 2005-2012 in companies from the European countries that are most suffering from the crisis.

In this sense, we conclude that the proactive environmentally-friendly actions carried out by the companies from Greece, Ireland, Portugal, Spain and Italy have not decreased during the crisis but rather that the crisis has meant an increase of environmental commitment. This has been strongly motivated by the Product Innovation actions which are the kind of actions which increase during the crisis. This is consistent with Porter and Van der Linde´s (1995) argument and is logical considering that during crisis periods companies have to be creative and adapt their products to the new situation which has more needs and less money.

Additionally, the behavior of the ER and RR actions is shown to be independent of the crisis.

The market (country), as well as the industry, has a significant effect on the Environmental commitment of these companies.

As a limitation of the paper, we should not forget that the study has been made considering the information disclosed by companies to ASSET4, and it would be challenging to analyze if this agrees with the real policies that they carry out. Furthermore, this evidence cannot be extrapolated to other countries with different characteristics (emerging countries, developing countries) or those which have been less affected by the crisis.

References

Albertini, E. (2013). Does environmental management improve financial performance? A meta-analytical review. Organization and Environment, 26, 431–457. [ Links ]

Al-Tuwaijri, A. S., Chistensen, T. E. & Hughes, K. E. (2004). The relations among environmental disclosure, environmental performance, and economic performance: a simultaneous equations approach. Accounting, Organization and Society, 29, 447-471. [ Links ]

Aragón-Correa, J. A. (1998). Strategic proactivity and firm approach to the natural environment. Academy of Management Journal, 41, 556–567. [ Links ]

Bansal, P., & Gao, J. (2006). Building the future by looking to the past: Examining research published on organizations and environment. Organization & Environment, 19, 458–478. [ Links ]

Baptista, C., Matias, F., & Valle, P. O. (2013). The moderating role of strategy and environment on the relationship between corporate liquidity and investment: evidence from panel data. Tourism & Management Studies, 9(1), 85-91. [ Links ]

Buysse, K. & Verbeke, A. (2003). Proactive environmental strategies: A stakeholder management perspective. Strategic Management Journal, 24, 453–470. [ Links ]

Charitoudi, G, Giannarakis, G. & Lazarides, T.G. (2011). Corporate social responsibility performance in periods of financial crisis. European Journal of Scientific Research, 63(3), 447-455. [ Links ]

Dixon-Fowler, H. R., Slater, D. J., Johnson, J. L., Ellstrand, A. E. & Romi, A. M. (2013). Beyond does it pay to be green? A meta-analysis of moderators of the CEP–CFP relationship. Journal of Business Ethics, 112(2), 353-366. [ Links ]

Ducassy, I. (2013). Does corporate social responsibility pay off in times of crisis? An alternate perspective on the relationship between financial and corporate social performance. Corporate Social Responsibility and Environmental Management, 20(3), 157-167. [ Links ]

Eisenhardt, K. M. (1989). Agency Theory: an assessment and review. Academy of Management Review, 14(1), 57-74. [ Links ]

Elkington, J. (1998). Partnerships from cannibals with forks: The triple bottom line of 21st century business. Environmental Quality Management, 8(1), 37-51. [ Links ]

Endrikat, J., Guenther, E. & Hoppe, H. (2014). Making sense of conflicting empirical findings: A meta-analytic review of the relationship between corporate environmental and financial performance. European Management Journal (in press). Retrieved November, 21, 2013 from http://dx.doi.org/10.1016/j.emj.2013.12.004. [ Links ]

Fernández, B. (2009). Crisis and corporate social responsibility: threat or opportunity? International Journal of Economic Sciences and Applied Research, 2(1), 36-50. [ Links ]

Grigore, F.G. (2011). Corporate social responsibility and marketing. In G. Aras, & D. Crowther (eds.) Governance in the Business Environment (pp.41-58). United Kingdom: Emerald. [ Links ]

Hart, S. L. & Ahuja, G. (1996). Does it pay to be green? An empirical examination of the relationship between emission reduction and firm performance. Business Strategy and the Environment, 5(1), 30-37. [ Links ]

Ioannou, I. & Serafeim, G. (2012). What drives corporate social performance? The role of nation-level institutions. Journal of International Business Studies, 43(9), 834-864. [ Links ]

Karaibrahimoglu, Y. Z. (2010). Corporate social responsibility in times of financial Crisis. African Journal of Business Management, 4(4), 382-389. [ Links ]

King, A. & Lenox, M. (2001). Does it really pay to be green? Journal of Industrial Ecology, 5(1), 105-16. [ Links ]

King, A. & Lenox, M. (2002). Exploring the locus of profitable pollution reduction. Management Science, 48, 289–299. [ Links ]

McWilliams, A. & Siegel, D. (2001). Corporate social responsibility: a theory of the firm perspective. Academy of Management Review, 26(1), 117-127. [ Links ]

Miller, J. L. (2002). The board as a monitor of organizational activity: the applicability of Agency Theory to nonprofit boards. Nonprofit Management and Leadership, 12(4), 429–450. [ Links ]

Miras, M.M., Carrasco, A. & Escobar, B. (2014). Are Spanish listed firms betting on CSR during the crisis? Evidence from the agency problem. Business and Management Research, 3(1), 85-95. doi: 10.5430/bmr.v3n1p85. [ Links ]

Molina-Azorín, J. F., Claver-Cortés, E., López-Gamero, M. D., & Tarí, J. J. (2009). Green management and financial performance: a literature review. Management Decision, 47(7), 1080-1100. [ Links ]

Orlitzky, M., Schmidt, F. L. & Rynes, S. L. (2003). Corporate social and financial performance: A Meta-Analysis. Organization Studies, 24(3), 403–441. [ Links ]

Pérez-Calderón, E., Milanés-Montero, P., Meseguer-Santamaria, M.L. & Mondejar-Jimenez, J. (2011). Eco-efficiency: effects on economic and financial performance. Evidence from Dow Jones Sustainability Index Europe. Environmental Engineering and Management Journal, 10(12), 1801-1808. [ Links ]

Porter, M. E. & Van der Linde, C. (1995). Green and competitive: Ending the stalemate. Harvard Business Review, 73, 120–134. [ Links ]

Ross, S. A. (1973). The economic theory of agency: the principals problem. The American Economic Review, 63(2), 134-139. [ Links ]

Russo, M. V. & Fouts, P. A. (1997). A resource-based perspective on corporate environmental performance and profitability. Academy of Management Journal, 40, 534–559. [ Links ]

Santos, J. R., Anunciação, P. F. & Jesus, M. M. (2013). Where stay social responsibility in economic and financial adjustments in Europe? Some questions aiming for an answer. In Santos, J.A.C., Perdigão, F. & Águas, P. Proceedings of the TMS International Conference 2012, Vol. 2: Human Resources, Business Ethics & Governance (pp. 664-674). Faro, Portugal: University of the Algarve. [ Links ]

Sánchez-Vargas, A. (2014). España vs Portugal: la imagen de ambos países y su evolución en tiempos de crisis. Tourism & Management Studies, 10 (Special Issue), 140-149. [ Links ]

Waddock, S.A. & Graves, S.B. (1997). Corporate social performance-financial performance link. Strategic Management Journal, 18 (4), 303-319. [ Links ]

Williamson, O.E. (1965). The economics of discretionary behavior: managerial objectives in a Theory of the Firm. Chicago: Markham. [ Links ]

Article history:

Received: 12 April 2014

Accepted: 16 November 2014